Stablecoins were crypto’s first scaled bridge to the real-world financial system. They worked because they solved several problems for different groups of people over the last several years: traders wanted stable collateral without leaving the chain, people outside the U.S. wanted access to dollar-denominated savings that their local banks couldn’t provide, and businesses wanted payments that didn’t take three days and cost three percent.

Stablecoins addressed these issues by offering a “programmable digital dollar” that settles globally, moves 24/7, and interacts permissionlessly with other assets on public blockchains. Stablecoins are a type of real-world asset (RWA) - an onchain instrument whose value references an offchain asset - and their adoption proved that tokenizing assets works at scale. They are the gravity pulling all of the world’s financial assets onchain.

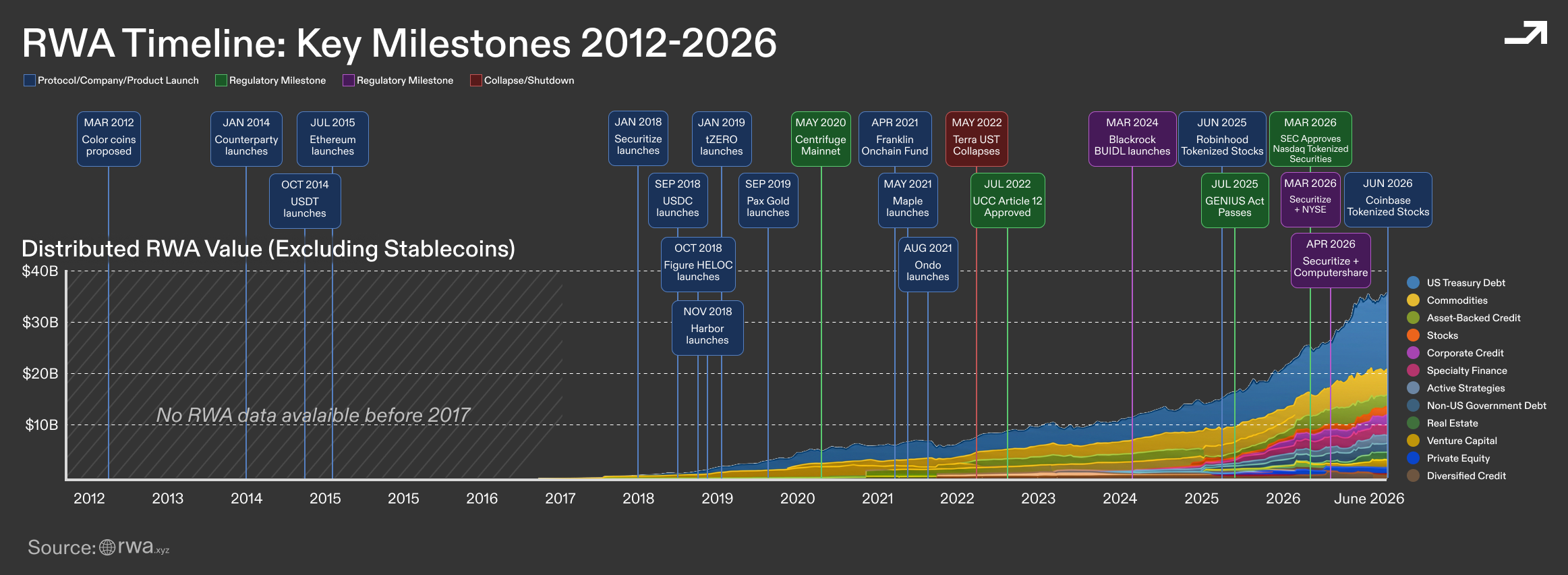

Today’s RWAs are a redux of the 2017-2020 Security Token and Alternative Trading System era. To understand why RWAs are being adopted today, one must internalize that blockchains are fundamentally a coordination and distribution technology. They do not manufacture demand where none exists, and there was simply no structural demand for the issuers and assets in that period.

There are several things that went right for RWAs over the last few years in addition to increased stablecoin supply. 2022-2024 saw a combination of crashing DeFi lending yields due to the bear market combined with rising Fed funds rates - this rate inversion rushed onchain capital into tokenized treasury products, which set everything else in motion. There was also increasing social acceptance with high-quality issuers such as BlackRock and Franklin Templeton, better infrastructure with embedded wallets and global on/off ramps, better DeFi primitives and participants such as vaults and curators, and greater regulatory clarity with GENIUS and a pro-crypto U.S. administration. Together, these ingredients have created an environment where both institutions and individuals are willing and able to allocate capital to a plethora of RWAs.

In this piece, I will:

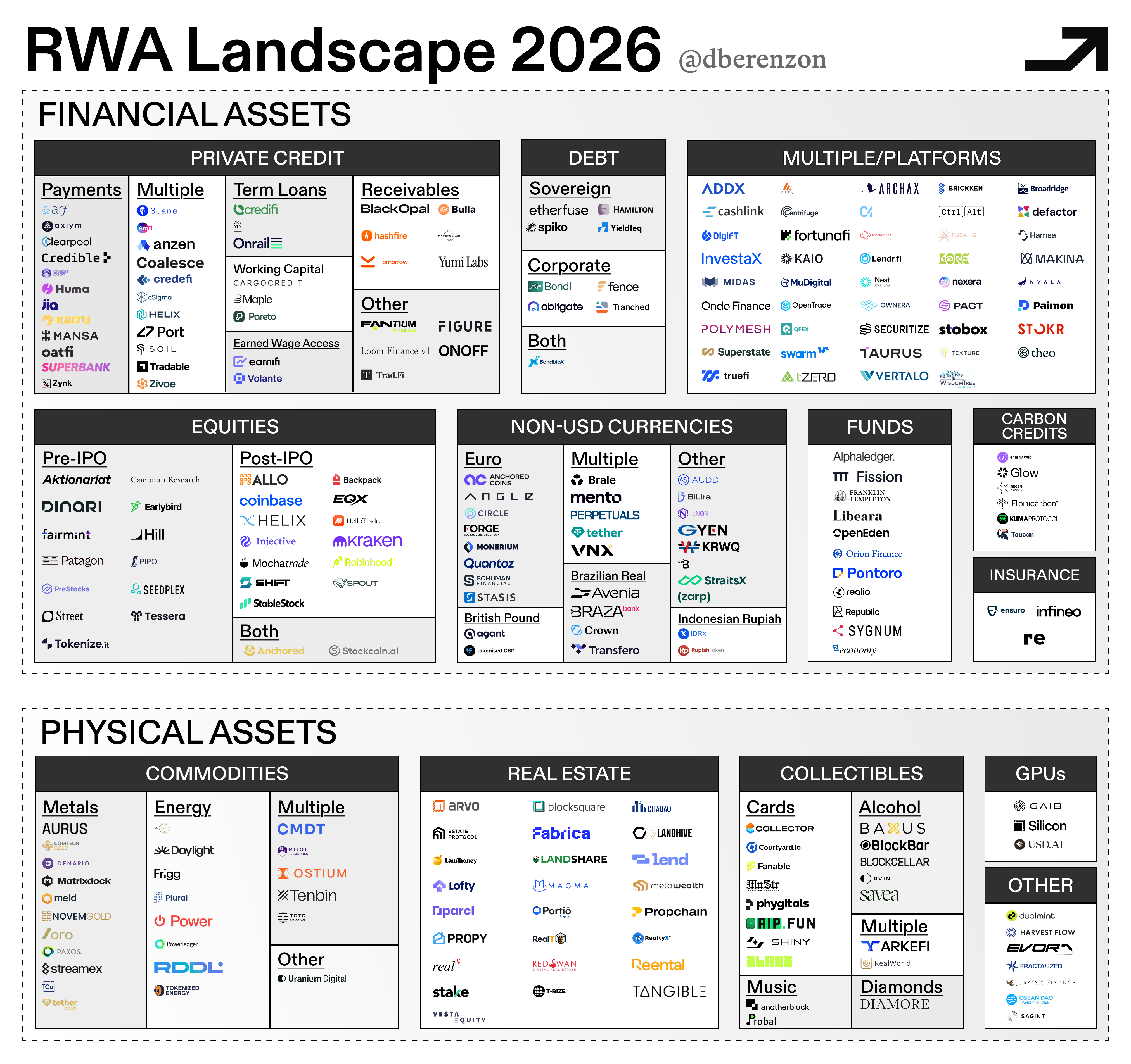

RWAs are an umbrella term encompassing dozens of structurally different instruments and sectors that share the property of representing offchain value on a public blockchain. Looking under the hood of an RWA reveals that each asset carries different legal rights, requires different infrastructure components, and offers different value propositions for investors.

We can examine an RWA through four different lenses:

THE REFERENCE EXPOSURE

The most important question is what economic exposure the RWA promises to deliver. There are two broad categories here - financial and physical.

Financial assets: Can be cash flows, equities, credit, currencies, or fund interests. Private credit is one of the largest and most heterogeneous categories, spanning from short-duration instruments, such as invoice factoring and merchant cash advances, to long-duration structures, such as project finance and term loans. Equities can be either public or private. Debt can be either sovereign or corporate. Funds can be either managed or passive. Currencies are straightforward in what they represent. There can also exist other forms of “exotic” financial assets, such as insurance and carbon credits.

Physical assets: Can be commodities, collectibles (yes, I consider Pokémon cards to be RWAs), and real estate, but there are also more exotic assets such as GPUs and mobility infrastructure.

Here is a more detailed taxonomy and market map:

An RWA may not perfectly track its reference exposure. A stablecoin depeg is the simplest example - a token might target one U.S. dollar but may trade above or below it. There are many factors, such as market closures, liquidity, issuer risk, oracle design, dividend treatment, and redemption friction, that can cause divergence.

THE VALUE PROPOSITION

We can categorize RWAs by the value that they provide for each side of the market.

As an issuer, you should consider who the holder of your asset is and why they may choose to hold the asset. As an investor, you should consider where the yield comes from and what your capital is going towards.

Cash Management: Offer users a conservative way to store value and earn yield. Sovereign debt, money market funds, and potentially AAA-rated corporate debt achieve this goal.

Financing: Channel capital to (and thus receives yield from) borrowers or originators, spanning short-duration payment and receivables financing through longer-duration corporate, real-estate, and project finance.

Market Access: Provide users with exposure to an asset they cannot easily access in their local markets because their local banking or brokerage companies either cannot or do not want to provide them. This can include equities, funds, and commodities.

Collateral and Composability: Often used inside other financial products, such as DeFi protocols for leverage and portfolio construction. Some can move permissionlessly onchain while others may only be transferable among whitelisted holders.

Trading and Hedging: Can provide long or short price exposure for directional trading or hedging rather than ownership of the reference asset.

Programmatic Administration: Leverage smart contracts to reduce costs associated with administrative functions such as issuance, subscriptions and redemptions, ownership and transfer records, and collateral management.

THE PRODUCT STRUCTURE

The reference exposure tells you what asset the RWA targets, while the product structure tells you how exposure is achieved.

There are several underlying components we can examine when considering an RWA as a product: the mechanism, the legal relationship, the denomination, the fungibility, and the user perimeter.

Mechanism

Single-asset tokens: Reference a specific share, bond, loan, commodity, or other asset. Buyers should be aware of the associated risks with each token structure and its associated issuer, and issuers should be aware of the legal requirements associated with these structures.

Pooled tokens or vaults: Pooled onchain deposit contracts that receive user funds and deploy them into one or more assets or strategies, either programmatically or through an active manager. Some may issue a transferable receipt token to the depositor.

Synthetics: Include perpetual futures, a CFD (Contract for Difference), a TRS (Total Return Swap), prediction markets, and other instruments that reference an asset without transferring ownership. The user owns a payoff rather than an underlying asset or claim on it.

Legal Relationship

There is a spectrum of “ownership” that an RWA provides a holder.

On the strongest end of the spectrum, the token represents the underlying asset itself and serves as the legally operative record of ownership (e.g. Superstate's GLXY). In other words, the legal instrument itself is issued and officially recorded onchain, and the blockchain is part of the authoritative ownership record rather than a representation of an offchain record.

On the weakest end, the holder receives a contractual payoff linked to the reference asset but has no ownership or beneficial claim on that asset (e.g. every perpetual futures contract).

In the middle, the token may provide a beneficial interest or redemption claim against assets held by an issuer, trust, custodian, or SPV (e.g. Tether’s XAUT). The token may also provide an issuer-backed contractual claim to the economics of the reference asset. For example, Ondo’s Global Markets tokens are fully backed total-return trackers designed to replicate the economics of owning the referenced stock; one token does not necessarily equal one share, and holders do not receive voting or other shareholder rights.

Denomination

Some RWAs represent a fixed unit of the reference asset, such as one equity share or one gram of gold. Others represent a dollar- or NAV-based interest in a pool. We often see the latter marketed as a “yield-bearing digital dollar” where the yield primarily comes from the underlying RWA.

Fungibility

U.S. dollars, common shares of Apple stock, and Treasury Notes with the same CUSIP are all considered fungible assets because all units of that specific asset are interchangeable with one another. Assuming they are tokenized in the same way, they can be represented as ERC-20s or a similar standard on a blockchain other than Ethereum. While real estate properties are obviously not fungible with one another and can be represented as NFTs/ERC-721s, the fungibility of the RWA depends less on the physical uniqueness of the underlying asset and more on whether the wrapper creates an economically identical claim, such as a real estate SPV issuing fungible shares.

A related concept is convertibility, which asks whether an RWA is directly interchangeable with the offchain asset. While most RWAs are isolated wrappers with their own liquidity and redemption process, some are attempting to allow conversion directly into the offchain asset. For example, DTCC’s planned tokenization service will allow securities to move between offchain (traditional book-entry) and tokenized forms while retaining the same CUSIP and rights. A major benefit of this is shared liquidity for both the onchain and offchain assets.

User Perimeter

Each RWA has its own mint, redeem, and transfer “perimeter”. For example, Ethena’s USDe can be minted by whitelisted users and companies who have passed KYC/KYB, excludes U.S. entities from minting, and is freely transferable onchain; while BlackRock’s BUIDL can be minted by U.S. institutions, has a $5 million minimum, and can only be transferred between whitelisted investors. Because of these nuances, even economically identical RWAs can still have dramatically different addressable markets.

THE ASSET LIFECYCLE

There are several steps in the life of an RWA, each of which introduces different service providers, risks, and operational requirements.

Origination

The underlying economic exposure of an RWA is created or acquired. Depending on the asset, this may involve originating a loan, purchasing securities or commodities, assembling a portfolio, or establishing reserves.

For heterogeneous assets such as private credit, real estate, and collectibles, the quality of the RWA is directly tied to how the underlying asset is sourced, evaluated, and structured. For private credit specifically, this includes underwriting standards, portfolio concentration, first-loss risk exposure, and recourse mechanisms. From a buyer’s perspective, this part of issuer diligence looks very much like traditional finance because you need to understand whether the originator is actually sourcing high-quality assets or simply selling adversely selected assets to onchain capital.

Enforceability

The intended economic exposure is translated into a legally valid claim. This is important because it determines the holder’s rights and recovery in stress, but it is also notoriously difficult to diligence. Problems for a holder arise when the underlying asset is already within a legal structure that has governance rights over it. For example, if the underlying shares of a tokenized pre-IPO stock are subject to issuer consent, rights of first refusal, lockups, or SPV-level restrictions, the token inherits those constraints. Furthermore, if the SPV manager of a pre-IPO vehicle learns that one of their investors signed a tokenization agreement with an issuer without the manager’s consent, they might take steps to remove the investor from the fund.

Issuance

This is the point at which the onchain asset is born. For permissioned RWAs, the investor typically first completes KYC/KYB, satisfies eligibility requirements, signs the relevant agreements, and has a wallet approved. The investor then sends fiat or stablecoins to the RWA’s designated offchain account or onchain smart contract. For offchain subscriptions, once payment settles, the issuer or their service provider uses the applicable reference price to calculate the token amount and authorize the mint to the holder’s wallet. For atomic onchain subscriptions, the smart contract checks eligibility and transaction conditions, pulls the payment, and mints the tokens in a single transaction; if any check fails, the transaction reverts.

Custody

The underlying asset is placed into an intermediary for safekeeping. This is particularly important for physical or reserve-backed assets because it directly affects how much the buyer trusts the issuer and how the secondary market prices the tokens. For example, a tokenized gold product must determine its vault provider and proof-of-reserves policy. As another example, a stablecoin issuer must figure out banking partner redundancy and reserve composition. Where possible, assets should be segregated and/or held in a bankruptcy-remote structure so that holders are protected from the insolvency of the issuer or other intermediaries.

Servicing

Many RWAs require ongoing offchain administration after issuance. For example, cash-flow-based assets, such as invoice factoring, require someone to collect payments, disburse funds, and manage defaults. If a borrower stops paying, a smart contract cannot programmatically collect from them. The more the administrative components of the RWA are offchain, the more a buyer should understand which service partners an issuer is using.

Pricing

Even though an RWA can trade permissionlessly 24/7, DEXs and CEXs are not the primary price discovery venues for any RWA asset today. While there have been cases of weekend price discovery for oil on Hyperliquid, it is immediately arbitraged back to the market price at market open. Pricing for opaque and slow-moving assets like pre-IPO shares and real estate will be more inaccurate and volatile, especially if the asset relies on appraisals, broker quotes, or secondary-market transactions. This is the biggest issue for holders of synthetic RWAs and leveraged products because a stale or manipulable oracle can lead to liquidations, poor execution with wide spreads, and dramatic downward repricing. There are additional nuances for public stocks, such as dividends and stock splits, that issuers and oracles must take into account.

Redemption

Eventually, the holder will exit their position. Upon redemption or maturity, the tokens are burned, the holder receives the proceeds or underlying asset, and any relevant offchain records are updated.

Think of RWA adoption as a cascade: a massive global pool of stablecoin capital seeking yield and utility flowing progressively into smaller asset pools as they build trust. The more “stablecoin-like” the asset pool is, the more liquidity it will amass. We can examine what this means through several characteristics:

DURATION

The quicker a stablecoin holder can get their money back for whatever reason, the more likely they will invest in the RWA. This naturally benefits RWAs with short durations and lock-ups. A 30-day lock-up for an invoice factoring vault is easier to swallow than a 3-year lock-up for a project finance vault. The longer the duration, the higher the yield must be to justify the liquidity gap. In practice, it is rare to find existing onchain capital comfortable with most opportunities beyond a 6-month lock-up, regardless of yield, due to perceived smart contract and execution risks.

One way to provide the experience of a shorter duration asset is to provide instant or gated redemptions. The larger the secondary market is for an RWA, the easier it is for an issuer to offer that option to holders. That said, if an issuer is promising instant redemption for a tokenized private credit fund with quarterly gates, they either have developed a strong secondary market with institutional investors and market makers willing to warehouse the risk, or they’re likely heading towards an asset-liability mismatch on their balance sheet. This often becomes a concern only during stress scenarios when many holders want out at once, but ideally a holder should understand the mechanism up front. This is even more important for unique physical assets, such as collectibles, because they have more edge cases around the implementation. For example, if you buy a tokenized PSA 8+ Charizard, do you have full redemption guarantees to receive that specific card and serial number, or does the issuer need to procure that card if you choose to redeem?

DISTRIBUTION

The closer an RWA “lives” to a liquid stablecoin, the less friction there is for users to swap their stablecoins into that RWA. This means that issuers who make their assets available on the major L1s and L2s, have liquid DEX pairs, allow users to hold and freely transfer assets across non-custodial wallets, and allow them to purchase assets via a one-swipe Apple Pay credit card on-ramp will find it easier to grow.

TRANSPARENCY

The more transparent an RWA, the more capital-legible it will be. Proof-of-reserves, audits, and attestations are all ways to ensure trust. This is especially true for pooled tokens and vaults since having the ability to examine a portfolio on a “look-through basis” allows holders to better understand the underlying assets, cash flows, and risks they are signing up for.

TRANSFERABILITY

Stablecoins are freely transferable onchain and can easily be used as collateral within DeFi protocols. They are digital dollars that can be put to work programmatically. The more an RWA resembles this property, the more useful and valuable it will be.

EXECUTION QUALITY

The easier an RWA is to buy and sell in size, the more likely it is to absorb stablecoin capital. While smaller buyers will likely stomach large spreads, poor depth, and stale pricing, larger buyers will simply revert to offchain venues for exposure.

The first asset type we’re already seeing being adopted is cash-equivalent assets - tokenized treasuries, money-market funds, and repurchase agreements. These are highly liquid, instantly redeemable, easily priced, and backed by high-quality institutional issuers. While many of these assets require KYC for minting, each has a slightly different architecture where the token can represent a fund share, beneficial interest, or other legal wrapper rather than direct ownership of an underlying security. These assets are great because they offer stablecoin holders a conservative yield option without forcing them back into the traditional banking system.

The next asset we’re seeing is asset-backed credit. I suspect this is because many of these opportunities are lower-risk by design due to the overcollateralization. Interestingly, the duration varies widely - loans behind Maple’s Syrup USDC usually have durations of around 180 days, while Figure’s HELOCs, which have seen a ton of growth over the last year, have durations of around 24 years.

While we haven’t seen this in the data yet, I believe we will see a wave of short-duration private credit come onchain, particularly for pre-funding liquidity for cross-border payments and credit card settlement.

We are seeing significant growth in a broad category of assets that can be considered “Access Products” - commodities, equities, and funds. One of the main benefits of RWAs is that they provide internet-scale distribution for high-quality assets, which is particularly helpful for wealth creation and preservation for individuals in countries with unsophisticated financial infrastructure. There are likely millions of people around the world who would love to own a share of Nvidia but do not have access in their local markets. Commodities like gold are also surprisingly difficult to access in many markets around the world but are highly desired by many people as an inflation hedge.

A helpful heuristic for RWAs is that the token generally inherits the underlying market's weaknesses. Real estate is the clearest example - minting an NFT representing a property does not remove the problems around title disputes, jurisdiction-specific transfer rules, and fragmented land registries. This type of asset will work best in jurisdictions where land registries legally recognize digital transfers, such as Dubai's initiative to record title deeds directly onchain. Pre-IPO equities face similar issues with offchain legal agreements (e.g. company ROFRs, as we’re witnessing today with the Anthropic SPV drama), and success with this asset class will largely depend on a company's willingness to tokenize its private stock. I believe that the companies most likely to do this will be consumer-facing products, marketplaces, and network-effect businesses more broadly because distributing shares can supercharge user growth and retention in the same way that network tokens have done to date.

Even though each asset category has broad properties, it is ultimately issuer-specific. Figure is a prime example here - few individuals in the world other than Mike Cagney could get lenders comfortable with a new HELOC originator, but I suspect that many have already worked with him at SoFi, which initially originated student loans that likely have similarly long durations.

It is often healthy to ask: “Where does the yield come from?”

For natively onchain assets and protocols, this usually comes from 1) someone selling a governance token somewhere (which includes token incentives), 2) interest rates from borrowers on lending protocols, and 3) trading fees for liquidity providers. For RWAs, the yield and associated risks are much less transparent. We’ve seen this vividly with early attempts at private credit, where the nature of the originators and borrowers came with adverse selection. When a borrower or asset has high yield, it can signal a pain point they face in receiving financing in the real world, but it can also signal that they are a higher-risk borrower. In other words, they may be willing to pay a premium because cheaper capital refused to underwrite the risk. This is less of an issue when the value proposition for a borrower is faster speed, cheaper cost, or increased supply from a global capital base via stablecoins.

While duration is one of the key components to yield, since investors generally require more compensation for a longer commitment, shorter duration does not necessarily mean lower risk. For example, private credit remains broadly exposed to macroeconomic conditions, and the underwriter's recourse muscle is a significant contributor to long-term performance.

Investors must not take an APY percentage at face value. They need a clear understanding of where the yield comes from, what risk they’re taking on, and how sustainable it is across different market conditions. The yield fairy is not real.

We have made a ton of progress since the 2018 security token era, but several gaps continue to limit mainstream adoption by both retail and institutional investors.

Reporting and verification remain opaque. Investors in private credit vaults should have better visibility into borrower profiles, outstanding loan balances, lending terms, and recourse status. For 1:1-backed assets, proof-of-reserves should be continuously posted onchain.

Oracle design for illiquid assets remains unsolved. We need better designs that account for private market data, infrequent price discovery, and wide bid-ask spreads. This is especially necessary for perps so that prices can be adjusted safely and accurately without liquidating users.

Vault curators need to be better stewards of capital. Curators are effectively performing an asset-allocation and diligence function, but the standards and accountability around that function remain underdeveloped. In traditional finance, similar responsibilities would sit within a regulated RIA, and ideally the curator function evolves towards that caliber.

Secondary market liquidity needs to deepen. Minting and depositing are much easier than supporting burns and redemptions, both at scale and during volatile market conditions. The reality is that secondary markets are non-existent for most RWAs today, and almost all liquidity currently comes from investors redeeming the asset directly through the issuer. That said, redemption facilities are popping up across the ecosystem that allow investors to exit for a fee and hold the asset until it can be redeemed. This is a positive development that will help jump-start the secondary market because it effectively provides a back-stop. Over time, these facilities will evolve into more robust and efficient clearinghouse-like solutions.

The last gap to mention is not infrastructure but rather regulation - unfortunately, most RWAs can't use the blockchain as the official record almost entirely due to the legal system. For example, as much as everyone touts BlackRock's BUIDL as the gold standard, the blockchain ledgers are not technically the source of truth. Yes, Securitize essentially updates their offchain ledger based on what's happening onchain, but it is the offchain ledger that will get held up in court. Ideally, we have more jurisdictions recognize blockchains as the official ledger.

Blockchains are the distribution channel for assets that previously had no way to reach users around the world, and for capital that previously had no way to reach assets around the world. They have enabled a class of digital assets - RWAs - that are easier to access, administer, finance, and utilize relative to their analog counterparts.

As issuers expand beyond stablecoins, I believe that trillions of dollars of assets will be tokenized over the next decade. The pace at which each asset gets tokenized will depend on how similar its properties are to stablecoins, as well as the underlying infrastructure, regulation, and market participants underpinning that asset.

Furthermore, the increasing availability of RWAs has laid the groundwork for a new wave of global neobrokers and asset managers. These platforms will leverage these assets to compete directly with local incumbents, offering global financial products to anyone with a smartphone and internet connection. Ultimately, this will lead to more democratized access to capital markets and economic prosperity for individuals around the world.

If you are building something in this space then please reach out on Twitter/X.

Many thanks to Yuval Rooz, Yuki Yuminaga, and Bryan Choe for their feedback on this piece.

—

Disclaimer:

This post is for general information purposes only. It does not constitute investment advice or a recommendation or solicitation to buy or sell any investment and should not be used in the evaluation of the merits of making any investment decision. It should not be relied upon for accounting, legal or tax advice or investment recommendations. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment or legal matters. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by Archetype. This post reflects the current opinions of the authors and is not made on behalf of Archetype or its affiliates and does not necessarily reflect the opinions of Archetype, its affiliates or individuals associated with Archetype. The opinions reflected herein are subject to change without being updated.

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

Unordered list

Bold text

Emphasis

Superscript

Subscript

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

Unordered list

Bold text

Emphasis

Superscript

Subscript

.png)