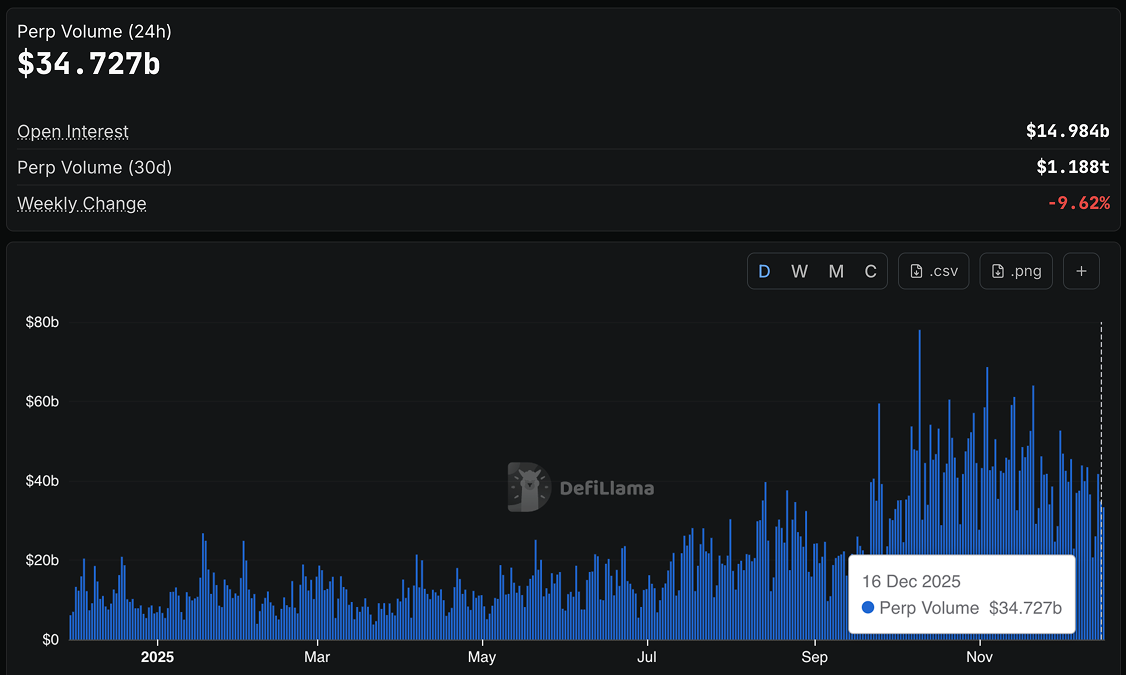

As of late, Hyperliquid’s revenue is down significantly from the millions to the hundreds of thousands in USD, and $HYPE has seen a sharp retrace of -50% over the last 2 months. But across the broader perp landscape, several protocols are still clearing $3B+ in daily volume and a tailwind of strong teams have yet to TGE.

Seeing this, some believe perps are topped, some believe that Hyperliquid is the end-all-be-all, and some just believe that perps as a primitive are inferior to instruments like options.

But I personally don’t believe any of that.

This is not the unwinding of a trade, but rather, the early days of a maturing and durable market.

If you have context on perps, skip to the next section. This article isn’t here to deep dive into how perps work, but rather to explain why it’s still early to make bets in this sector.

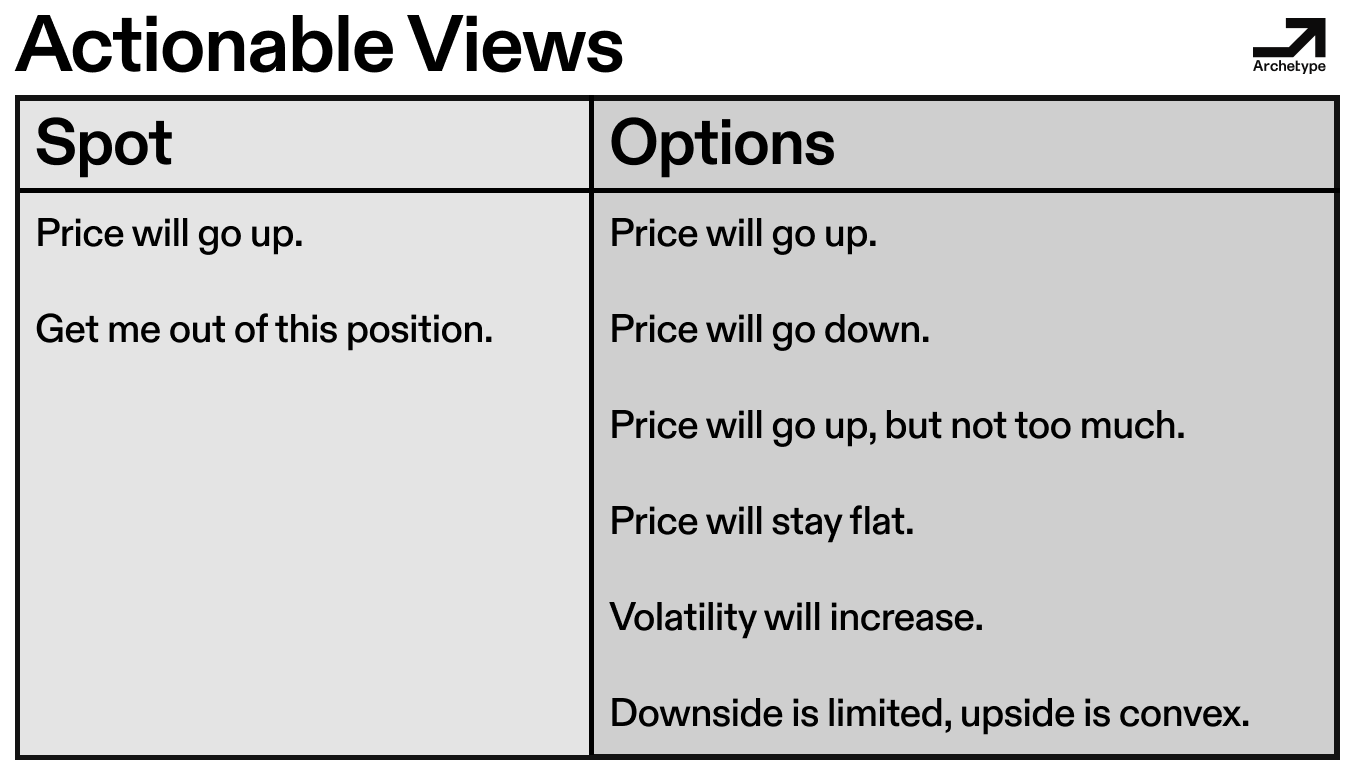

Let’s say that you’re bullish on Bitcoin.

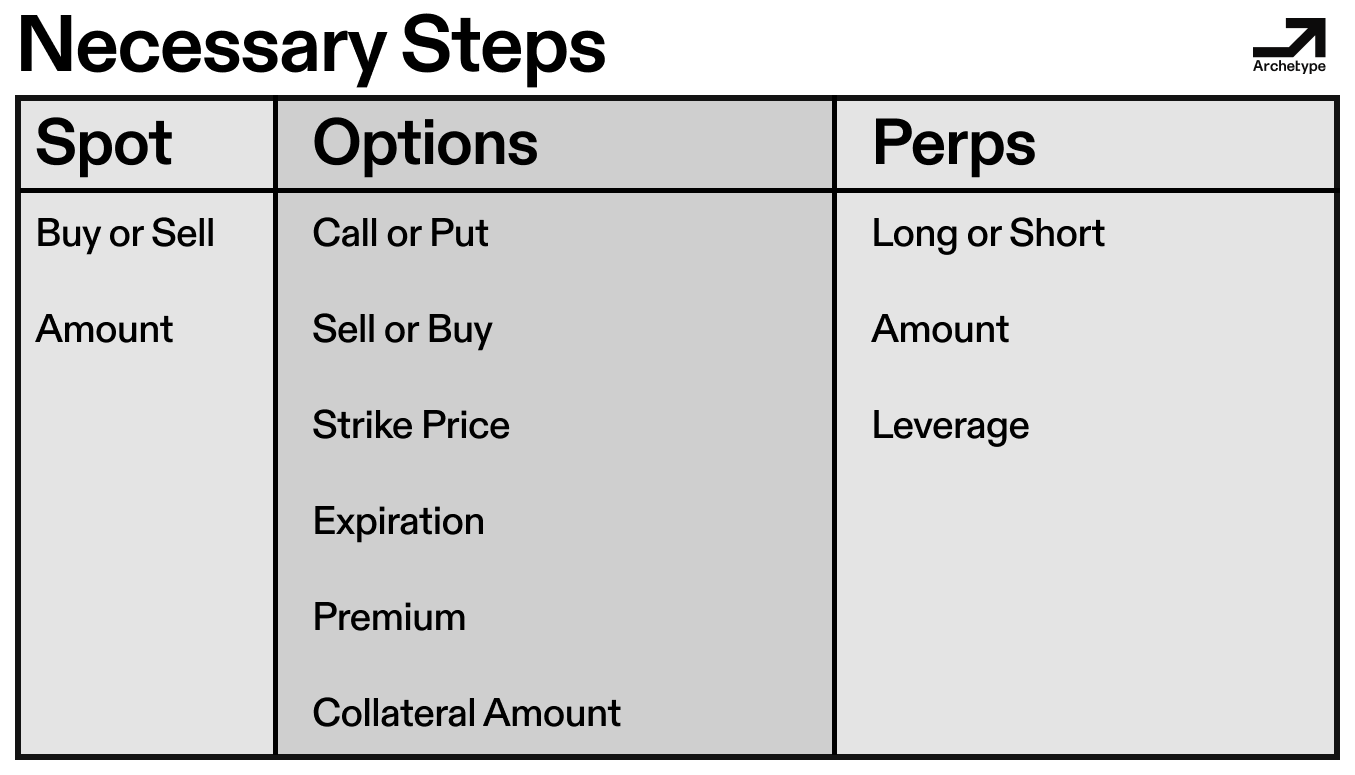

The most intuitive step you can take to gain exposure would be to buy 1 BTC, hold it as the price goes up, and sell it before the price goes down. This is spot trading in its simplest form. Spot is useful for owning assets in large size throughout prolonged periods, but it alone cannot fulfill all intents traders wish to express.

What if you wanted to bet on your belief that ETH is going to 0, but most of your money is still stuck in that 1 BTC you bought earlier? This is where contract-based derivatives like options come in. Options are a more dynamic form of trading that allow you to act on more views, like how much risk to take, how much capital to use, and what direction you want to bet in (long if you think price is going up, short if you think price is going down).

In this case, you can put what little capital you have left into selling an ETH call option, which gives you implied leverage, or more underlying exposure for less upfront cost. Introduced in 1973, options have become extremely popular in traditional finance markets and are much more dynamic than simple spot trading. But with that dynamicity comes complexity: you must choose a strike above spot, select an expiry, post margin, and actively manage the position by buying back the call to lock in profit or limit risk.

Yeah, it’s confusing.

Looking to bridge the gap between the intuitive UX of spot and the capabilities of options, Arthur Hayes popularized the concept of perpetual futures, or perps, with the launch of Bitmex in 2016. Perps gave us the functionality and advantages of options, but with the simple, familiar UX of spot.

As a perps user, you simply choose to long or short and choose how much leverage you want. In our prior example, we can achieve our intended outcome with perps by placing a short on $ETH: we just select how much money (margin) we want to put up and how much leverage we want.

Despite their simplicity on the surface, perps have evolved into a multi-billion dollar sector that is used not just for directional bias, but also for complex pair trade strategies onchain.

One of my favorite examples are pre-market perpetuals, which cover tokens that are otherwise not yet tradable on markets. These venues have found themselves clearing $20M+ in hour-one volume on platforms like Hyperliquid. Take the Plasma launch as an example: an ICO participant with a $1B entry may want to lock in an advantageous price by placing a short at $12B and capturing the spread as prices equalize.

We are also seeing more secondary-market token holders choose to hedge off their risk via perpetual instruments. This could be a firm acquiring locked over-the-counter tokens and shorting on Hyperliquid, a fund selling out of a locked position by shorting, or a trader hedging future airdrops.

When you step back and look at perps as an instrument, it becomes clear that the product simply fits well with the market. Perhaps volumes and recent data don’t reflect this yet, but underwriting a longer-term category requires understanding the relevancy and defensibility of its core product. Built on funding rates and onchain orderbooks, perpetuals have become something users actually want: a simple primitive that allows traders to take leveraged long or short exposure on an asset without expiry.

The rest of this article will cover three main philosophies that drive my thesis around where perp DEXs (decentralized perpetual futures exchanges) are at and the growth they still have ahead of them. This is to say that we’re not at the top just yet.

I know this seems like a headline that is too obvious to be taken seriously, but this is a fairly recent trend in crypto. So what happened and why now?

Over the past two years, a consensus has formed that buy-side pressure and retail engagement have slowly been 1) absorbed by hyper-speculative assets like memecoins and 2) withheld by more sophisticated and skeptical crypto traders.

For years, the simple BTC-to-altcoin-to-BTC rotation was a reliable strategy: if BTC went up, you’d just buy the cheapest alts most relevant to the biggest narratives at the time. So in 2025, when BTC went up, traders bought FARTCOIN, VIRTUALS, and GOAT. In 2024, BTC went up, and traders rotated into SUI, SEI, and TON. In 2021, it was ARB, OP, and ETH.

Those types of generalized L1s and narrative-driven tokens are no longer attracting the same type of demand in today’s markets. For many would-be buyers, it is difficult to justify how value accrues to most tokens and how the underlying businesses make money in the first place.

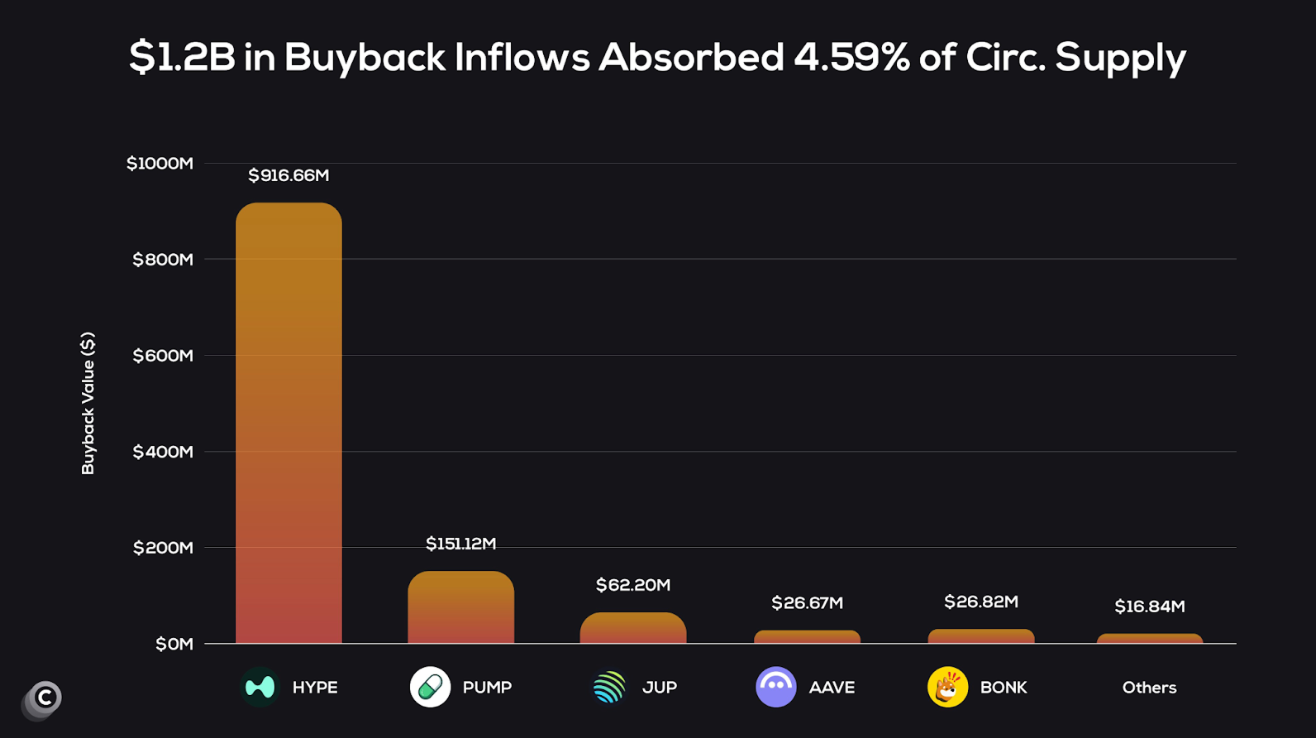

This all changed when Hyperliquid, an exchange which allows users to trade perpetuals onchain, disrupted the market with a value accrual program known as a buyback. This is a mechanism by which a protocol allocates a portion of their revenue to buy back into their associated token, more concretely tying the business and, most importantly, its revenues to the token. Buybacks have certainly existed prior to Hyperliquid, but the perp DEX’s recent incorporation of them is the most successful implementation of buybacks to date. And a lot of that is because of Hyperliquid’s clear revenue generation as a business.

But of course, this reflexivity risk works both ways. Buyers often feel more comfortable investing into a token with buybacks if they can see a clear price-to-revenue expectation, but they’ll similarly be less inclined to invest if the business is not maintaining consistent revenue numbers.

A clear example of this is Pumpfun and their numerous buyback programs, which have not prevented their steep -70% decline since ATH in August of 2025. For buybacks to work, protocols need to clearly explain and demonstrate how the underlying business works and how long it will last. In Pumpfun’s case, the memecoin market dropped by over $100M in volume over the last 3 months, and their $205M worth of buybacks couldn’t keep their token holders from selling.

Pumpfun is an example of how concerns around the longevity of memecoin markets unsettled investors even when there were buybacks. Their particular fear is that the decreasing memecoin volume will give way to decreasing revenue numbers, which will reduce the amount of money going into buybacks and, ultimately, negatively impact the price of the token.

In contrast to the memecoin market, perpetuals have increasingly grown in popularity as a durable trading infrastructure less exposed to short-lived dynamics, and are instead more aligned with long-term macroeconomic sentiment. Developments like Coinbase launching their own perp exchange reinforce this shift, validating perps as a core component of the modern-day trading stack as opposed to a trendy sector.

The market is now betting on long term cash-flow, and perp exchanges fit the bill as one of the strongest onchain businesses. You may have missed the initial wave, but in a liquidity-desperate market like crypto, it is hard to bet against a real business like perps.

As a fund that holds $HYPE, we at Archetype optimistically see Hyperliquid charging forward as an index and category leader for perp DEXs. With Hyperliquid’s focus on infrastructure, it has the potential to become a primary onchain venue much like how Binance is quoted unilaterally against CEXs.

But that doesn’t mean they’ll be the only player.

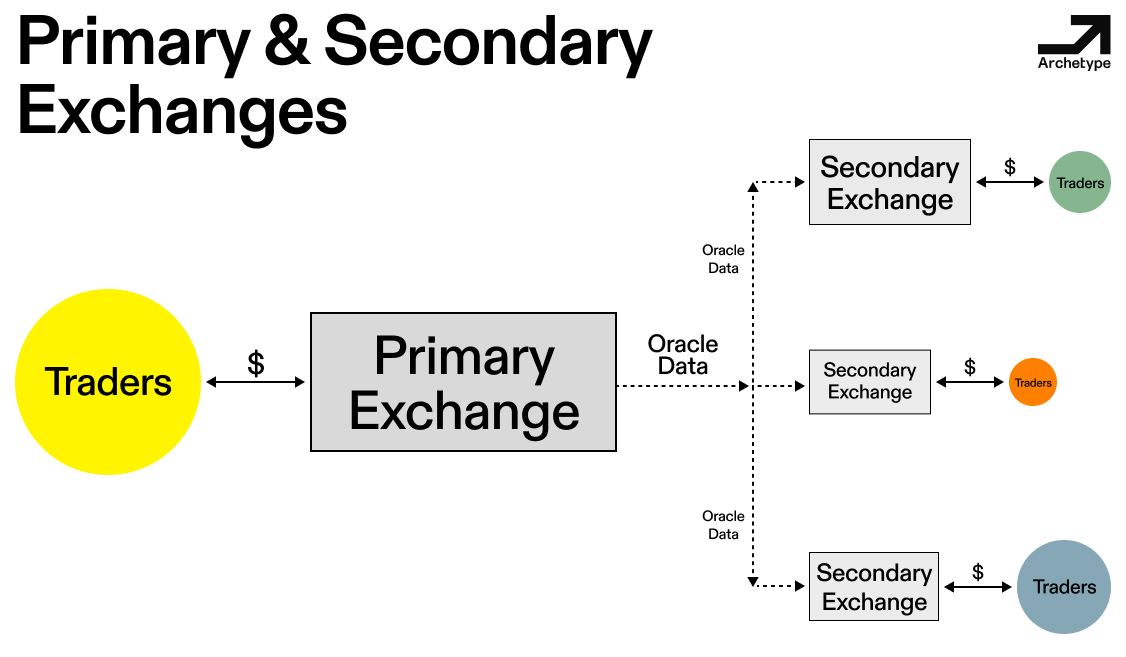

In any trading market, there is a natural bifurcation between the primary and secondary exchanges. Primary exchanges are the main and most attractive venues for a trader to contribute liquidity to, resulting in their power to “discover price.” This means that, for the most part, a primary venue is the market’s main reference point. On the contrary, secondary exchanges are responsible for distributing access to that price.

This structure is what allows for an efficient market where all traders have access to exchanges with adequate liquidity. So while they’re often overlooked, secondary venues are absolutely necessary for the market to grow.

Hyperliquid may have led the way, but billions of dollars in perp volume have flowed in from tailwinds like Aster, Lighter, and EdgeX. Even if you missed Binance, having early investments into “runner-ups" like Upbit or Coinbase would have yielded profitable returns. The same will be true for many secondary perp exchanges.

Like with any new space, everybody implicitly wants to just back up the truck on a primary winner. If you believe that Hyperliquid will become the primary onchain venue, then bidding at $26B FDV is cheap.

My argument is that secondary venues have separate valuable purposes, even if some are just inefficiently relying 1:1 on prices straight from Binance. For example, Upbit captures a heavily regulated $1.5B of spot trading volume from Korean retail. That might be meager relative to Binance, but crypto projects continue to fight for spots as KRW listed pairs, and Upbit’s valuation in secondary markets is currently around $10B.

On the perp DEX side, Aster is the comparable case study of a secondary venue that saw success by providing a Binance-affiliated perp DEX to retail traders. As of mid-December 2025, Aster still holds an impressive $2.5B in open interest thanks to its extension of the Binance brand and token-listing process.

Secondary venues can carve out value by focusing on capturing different trader bases via two main moats: different branding and different asset types. Winning market share by cornering a separate long-tail asset is still a durable long term business. In the current CEX market structure, this would be MEXC and their willingness to list more risky assets, which allows it to clear $3B in daily spot volume.

If you are going to take a long-term bet on a perp DEX, you need to distinguish between whether they will successfully become a primary venue or set themselves apart as a defensible secondary exchange.

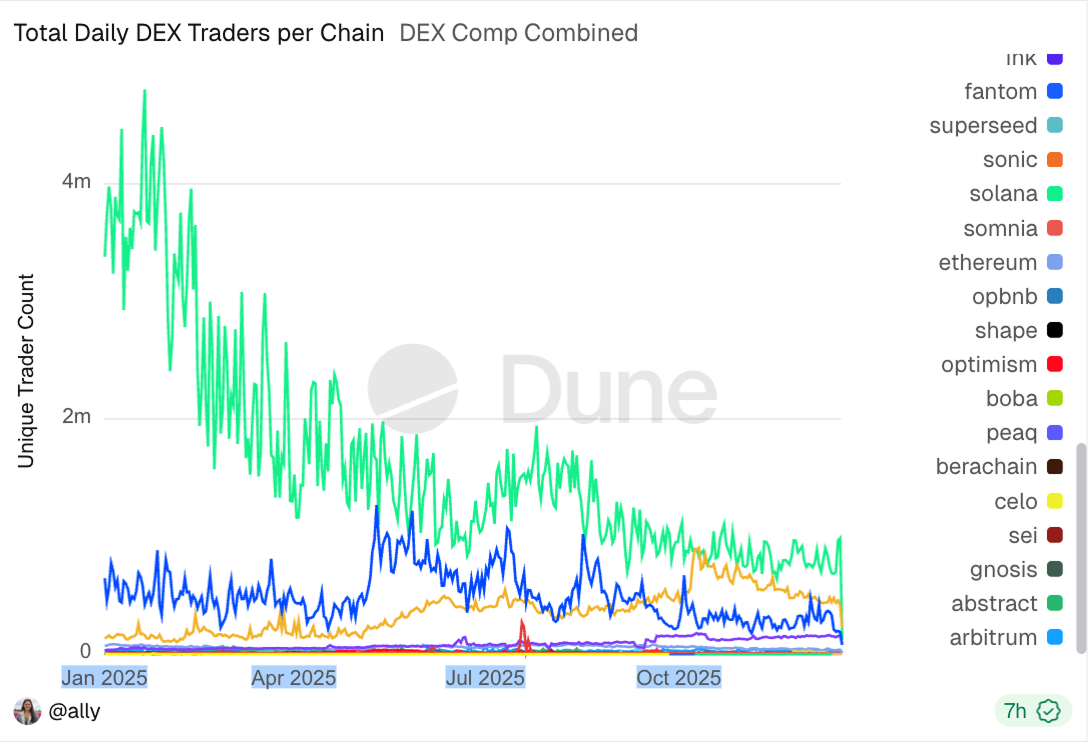

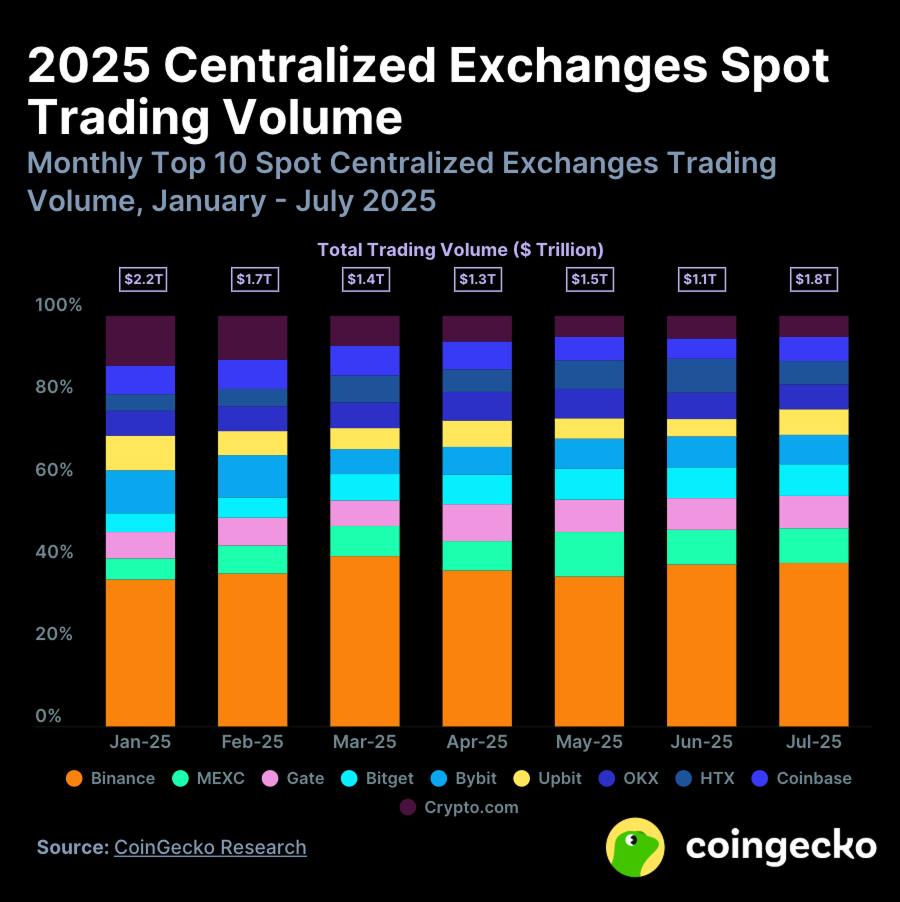

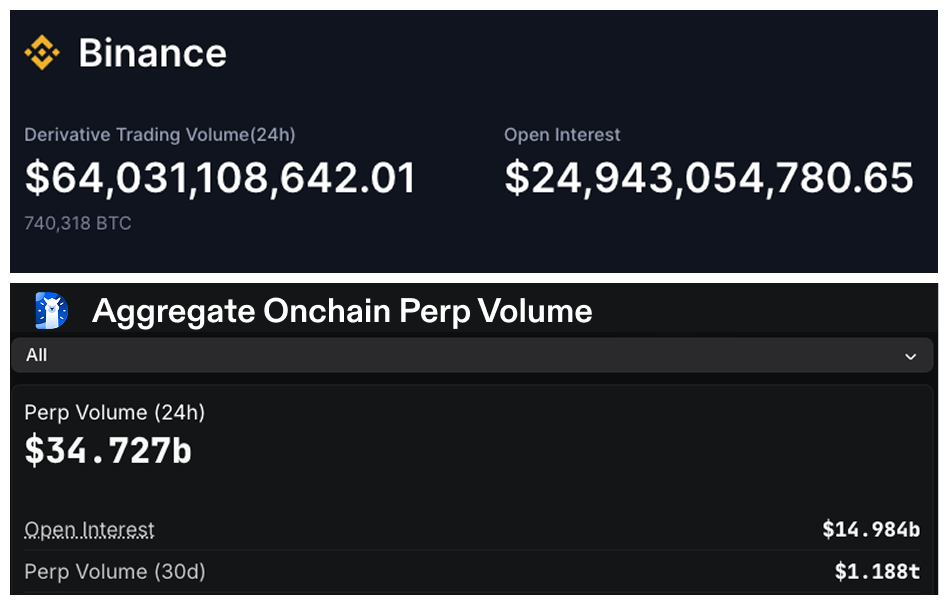

When you zoom out, the overwhelming majority of derivative activity still happens offchain. Centralized exchanges process trillions in annual perp flow and continue to dominate with respect to liquidity, user counts, and market depth. In fact, Binance alone does more perpetual volume in a day than the aggregate daily volume of the entire onchain perp DEX sector!

This is billions in offchain volume that continues to congregate at a singular primary venue, demonstrating that onchain perps still have a long way to go and have plenty of liquidity to onboard. The main constraints (and opportunities) to change this and bring that volume onchain can be categorized into what we call push factors and pull factors.

Let’s start by defining the main pushes that drive volume away from onchain perp solutions.

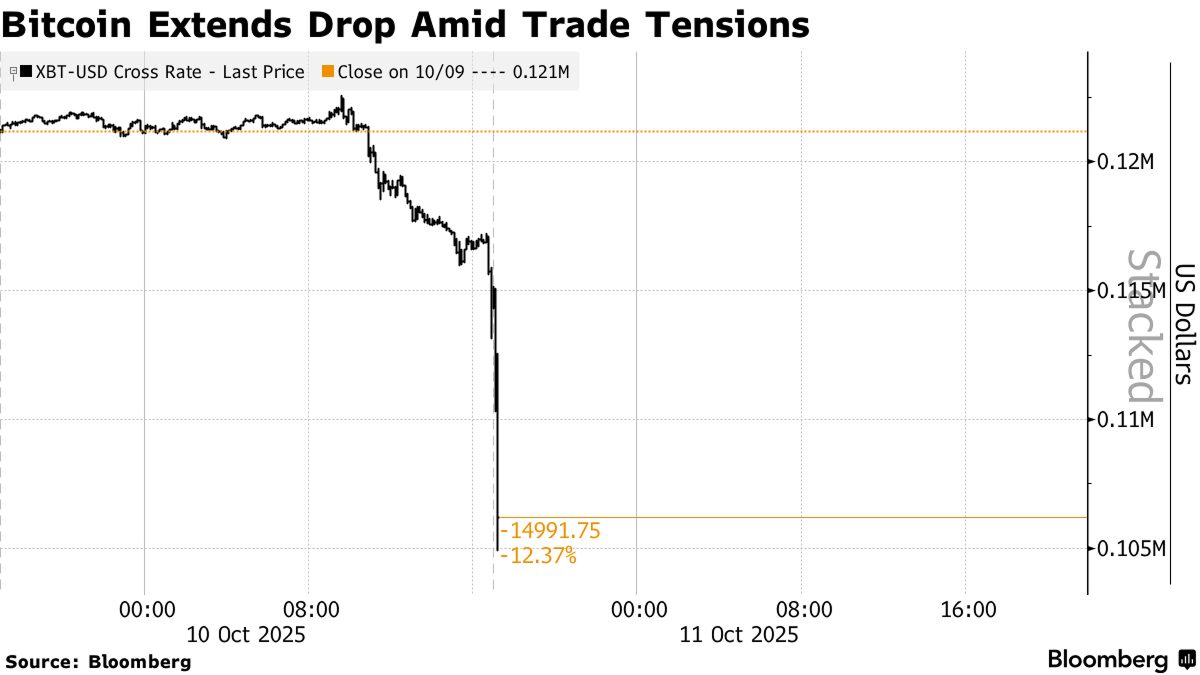

There is no better event that highlights the glaring immaturities in perps than the recent incident on October 10th, 2025. This is the largest crypto market crash we have seen to date, where Trump’s 100% tariff on China sparked a $19B crypto liquidation cascade.

To understand the crux of this issue, we need to talk about oracles, which perpetual setups rely on heavily to create their markets. These oracle-to-perp-market pipelines aim to replicate an asset’s price as closely as possible to its supposed true price. In an ideal setup, the pipeline will take into account a diverse set of sources—from primary spot exchanges to various secondary venues—in order to calculate a reference price for these synthetic markets to anchor on.

A perpetual market uses this indexed price along with measurements of supply and demand to ultimately determine the mark price, which is the main metric that we trade on, calculate PnL from, and liquidate at.

Creating and setting a mark price isn’t exactly foolproof yet. How these mark prices are calculated and indexed can make the difference between a robust market with consistent prices, or one that is vulnerable to manipulation.

In the case of the 10/10 event, Binance’s oracle suffered a failure and propagated an incorrect USDe price. The error cascaded across many exchange venues, heavily impacting those who relied on Binance for mark pricing.

Some of these exchanges triggered auto-deleveraging (ADL), which is a fail-stop that closes profitable positions in order to prevent the entire system from going insolvent. HLP (Hyperliquid’s vault) successfully absorbed hits, but LLP (Lighter’s vault) took a -5% drawdown. Other concerns ruminated across the space as traders argued whether or not Hyperliquid’s ADL was fairly designed and executed, as it sorted through high-profit and high-leverage positions and closed them in order.

Oracle problems are just one of a handful of critical issues that perps still face. While CEXs have historically solved for this with scale and liquidity, their structure requires unavoidable control that introduces other risks.

For onchain perpetuals, teams that solve these push factors can attract dormant and competitive liquidity, resulting in meaningfully deeper books that can handle future cascades like that of 10/10.

At a structural level, CEXs cannot list every asset or market that traders request. They need to protect their brand, they need to abide by their jurisdiction’s regulation, and they need to be careful what they promote to traders.

Inversely, onchain perpetual platforms create transparent and programmable systems that eliminate the brand risk constraints that can often prevent expanding markets. There is transparency around how mark price is calculated, what weightings index price has, and how assets are listed.

These transparent systems are a key advantage and enable onchain perps to create exotic long-tail markets. Pre-IPO markets, tokenized equities, or even synthetic assets like Pokémon cards are all examples of unique markets that corner long-tail consumer groups and pull them into using perps.

In my eyes, the best way to approach onchain perpetuals is to find solutions that either focus on diminishing the push factors or increasing the pull factors.

Whether it is improving funding rate systems or introducing new synthetic markets, perps are still early enough where there are enough problems to be solved and potential in the market to make bets on. Onchain volumes are clearly not at par yet, but all it takes are a couple teams to plug the right holes and create the right markets.

To say derivative contracts have exploded this year would be an understatement. Perpetuals have evolved the modern-day trading stack into a market where traders can be as diverse as they’d like while still using simple, familiar instruments.

New projects want perp listings, they want higher volume numbers, and they want to distribute their token through more venues. Whether offchain or onchain, perpetual exchanges continue to clear billions of dollars in daily volume.

I believe that the future of perpetuals belongs onchain, and when looking through the crowded landscape of projects, I’m focusing my attention on teams creating new high-demand markets or solidifying primary venue infrastructure.

Yes, there will be a few major winners. But there will also be room for players who want to expand the market with differentiated asset types or uniquely solve certain inefficiencies.

If you are building an onchain perpetual protocol and still believe we are early, then please reach out to me on Twitter at @thatdegenvc.

Thank you to Taetaehoho, Sam Ruskin, Mikey, Rui, Poopman, Aadharsh Pannirselvam, Danny Sursock, Katie Chiou, Dmitriy Berenzon, and Tyler Gehringer for your research, support, and inspiration on this piece.

*denotes an Archetype portfolio company

—

Disclaimer:

This post is for general information purposes only. It does not constitute investment advice or a recommendation or solicitation to buy or sell any investment and should not be used in the evaluation of the merits of making any investment decision. It should not be relied upon for accounting, legal or tax advice or investment recommendations. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment or legal matters. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by Archetype. This post reflects the current opinions of the authors and is not made on behalf of Archetype or its affiliates and does not necessarily reflect the opinions of Archetype, its affiliates or individuals associated with Archetype. The opinions reflected herein are subject to change without being updated.

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

Unordered list

Bold text

Emphasis

Superscript

Subscript

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

Unordered list

Bold text

Emphasis

Superscript

Subscript